1300 13 22 77

1300 13 22 77

Split Home Loan

Get a Fixed & Variable Loan

Split loans let you fix part of your loan and stay flexible with the rest with a variable rate.

What’s a Split Loan?

A split home loan means part of your loan has a fixed interest rate, and part has a variable rate. It’s like having two mini loans in one. The fixed part gives you stability, you know exactly what your repayments will be. The variable part gives you flexibility, you can make extra repayments, redraw money, and benefit if rates go down. You get the peace of mind of fixed, with the freedom of variable, all in one loan.

How can you split it?

You can split your home loan however you like, 50/50, 20/80, 70/30. It really depends on what you’re comfortable with and how you would like to repay your loan. Here’s an example of how you can divide your payments, the example is for a $500,000 loan (Fixed rate is 4.99% and Variable rate is 5.59%*).

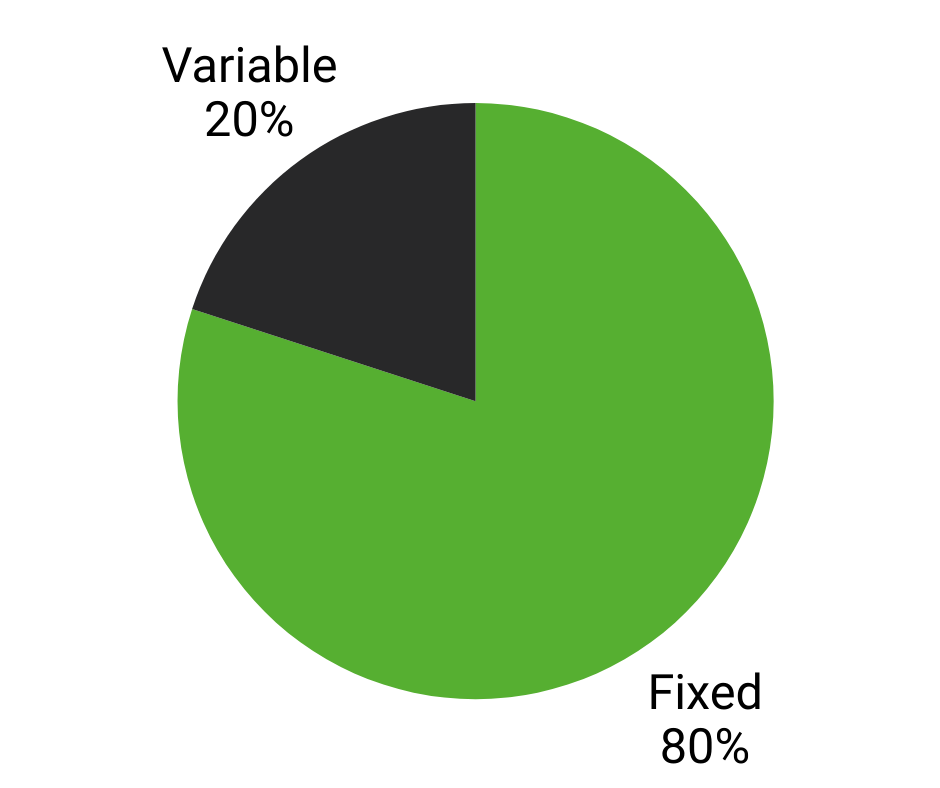

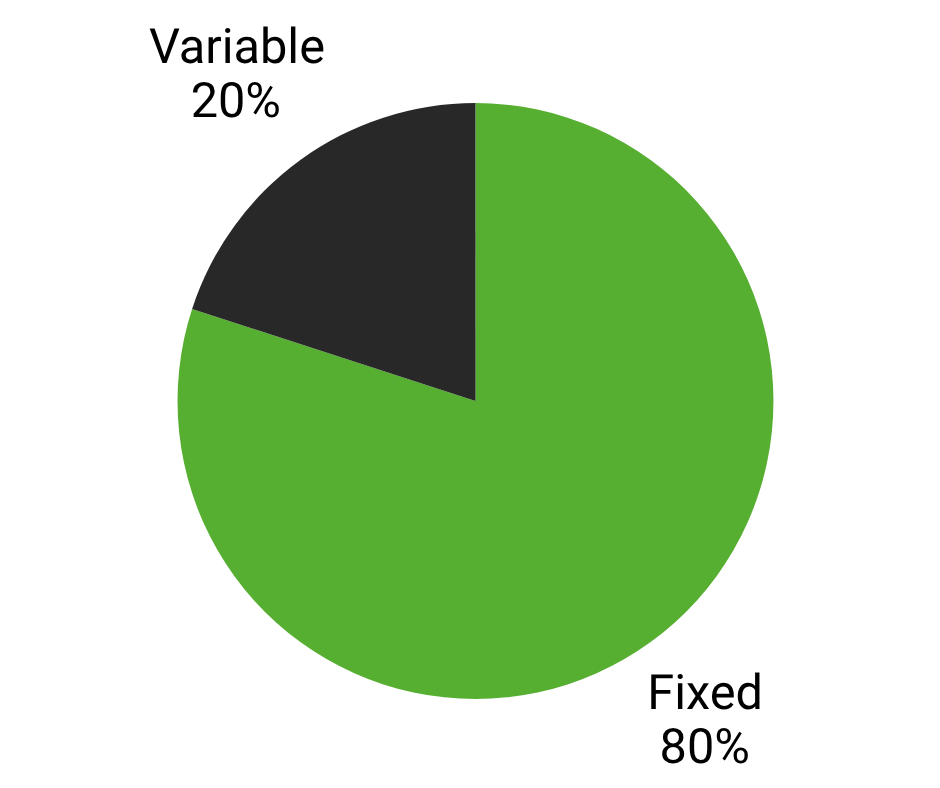

20 / 80 Split

Fixed Portion: $400,000

Variable Portion: $100,000

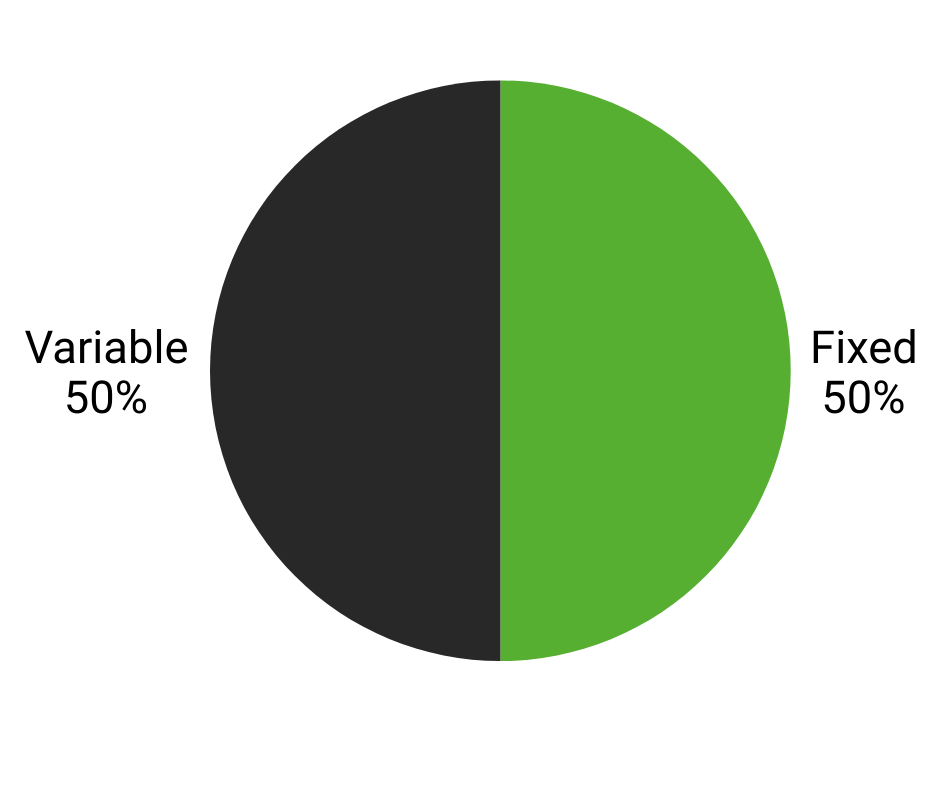

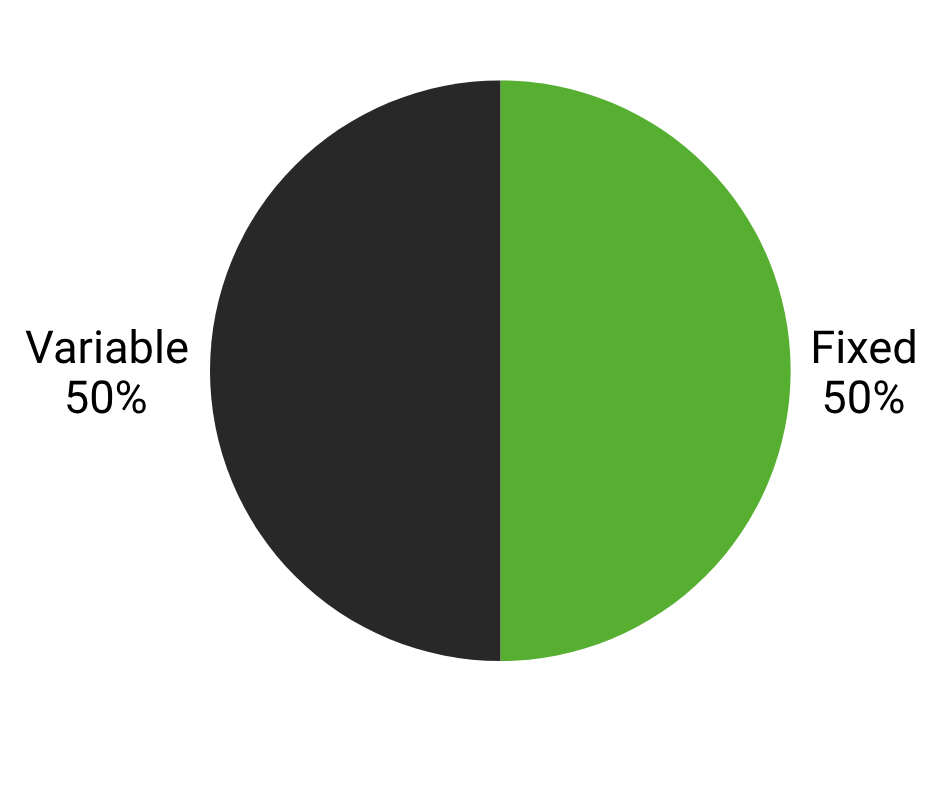

50 / 50 Split

Fixed portion: $250,000

Variable portion: $250,000

30 / 70 Split

Fixed portion: $150,000

Variable portion: $350,000

Choosing a split is about more than just repayments, it also depends on your risk appetite, flexibility needs, and view on future interest rates.

*These figures are estimates only and don’t include fees or charges that may be applicable. Please talk to a Mortgage Specialist if you would like to consider your personal situation and needs.

Peace of mind

Enjoy repayment certainty, the fixed portion of your loan gives peace of mind with predictable repayments which is helpful for budgeting.

Flexible

The variable portion allows extra repayments which could mean you can pay down your loan faster.

Protection

The fixed portion shields part of your loan from sudden interest rate increases.

How to apply

You can apply over the phone or by visiting one of our financial services stores. One of our Mortgage Specialists will guide you through the process.

Frequently asked questions

You get the certainty of fixed repayments on one portion while maintaining the flexibility to make extra repayments or use an offset account on the variable portion. It can help manage risk when interest rates are changing.

It depends on your financial goals, risk tolerance, and need for flexibility. For example, if you value stability, you might fix a larger portion. If you plan to make extra repayments or use an offset, you may prefer a larger variable component. It is best to speak with a Mortgage Specialist about your personal situation and this may impact your decision

You can make extra repayments, access redraw and pay out early without penalty on the variable portion. But this does not apply to the fixed portion of your loan

Yes, the variable portion allows an offset account, which can reduce the interest you pay. The fixed portion doesn’t have offset access.

No, you won’t pay double fees for a split loan, it’s treated as one loan account with two sub-portions.

Yes, you may be able to restructure or refinance your split loan. Keep in mind that breaking a fixed term early could trigger break costs.

Our fixed terms range from 1 to 3 years. After the fixed period ends, that portion will usually revert to a variable rate unless you refinance or re-fix.

Yes, many property investors use split loans to balance cash flow certainty with flexibility to pay down debt faster or use offset features.

You can view Target Market Determinations here .

*These rates are for a demonstration purposes only and are not to be used as reference for your own split loan consideration. Please refer to our Home Loan product pages for up to date and current interest rates and comparison rates.